This is Part One of a 3-Part Blog Series.

Today, the Union of Concerned Scientists released an update of our 2012 ground-breaking analysis, Ripe for Retirement, examining the economic viability of U.S. coal generators compared with modern, cleaner alternatives. Our new findings, published in Electricity Journal, show that nearly 59 gigawatts (GW) of coal power capacity are not cost competitive when compared with natural gas, and more than 71 GW are uneconomic when compared with wind power. These coal generators are prime candidates for retirement and their closure would provide substantial benefits for consumers and the environment. It would also accelerate the transition to a cleaner, more reliable and affordable energy system.

Coal in Decline

As I discussed in a recent blog, the U.S. coal power industry has been in decline for several years now. Coal-fired electricity fell from about half of U.S. generation in 2008 to 37 percent in 2012. Going back to 2009, nearly 21 GW of coal power capacity has already retired (6 percent of the U.S. coal fleet), and another 34 GW of coal generators has been announced for closure. This includes several high profile announcements made in 2013 by major power providers, including Georgia Power, American Electric Power, and most recently, the Tennessee Valley Authority.

Collectively, these decisions are part of the dramatic transition underway in the U.S. power sector, in which old and inefficient coal units are being retired in favor of cleaner energy sources like renewable energy, energy efficiency, and natural gas. And considering the state of the remaining coal fleet, along with current market and policy dynamics, many more coal retirement decisions are likely on the horizon.

Our Economic “Stress Test”

We updated our analysis because the U.S. electricity market is constantly changing and a fresh look was warranted. For both the 2012 report and the current analysis, we employed a simple economic “stress test” to evaluate the competitiveness of coal generators. In short, we estimated a coal generator’s operating cost—after being upgraded with modern pollution controls—and compared it with the average cost to generate electricity from several alternatives, including existing and new natural gas combined-cycle (NGCC) power plants and new wind power facilities. If the coal generator’s costs were more expensive, then it failed our test and was deemed ripe for retirement.

For our new analysis, we made several important modifications, which included using the latest available annual data for the coal fleet (2011 instead of 2009 data from the original study), updating cost and performance assumptions for natural gas and wind, and refining our methodology to provide for more regionally-specific results.

Midwest and Southeast States Lag Behind Again

When compared with natural gas, 329 coal-fired power generators in 40 states — representing 58.7 GW of power capacity — failed our economic test (see map). This total includes 69 coal units (17.8 GW) that are new to our ripe for retirement list for this 2013 update. That finding demonstrates very clearly that the coal fleet’s ability to compete economically with cleaner alternatives has further declined since our original analysis.

Many Ripe for Retirement Coal Generators are located in the Midwest and Southeast.

More than half of the ripe for retirement coal units were located in the Southeast or the Midwest. In fact, these two regions are home to all of the top 10 states with the most ripe for retirement capacity.

Michigan now ranks first in the country with the most ripe for retirement coal generation capacity, up from the number five spot it occupied in the original analysis. This is due to an additional 10 coal units flagged as ripe for retirement under our updated analysis, which increased Michigan’s total from 3,648 MW of power capacity to 6,719 MW.

With some of the highest electricity prices in the country, retiring this uneconomic coal would benefit Michigan consumers. To ensure that clean energy sources play a dominant role in replacing this coal generation, Michigan’s Governor and legislature need to strengthen the state’s renewable energy and energy efficiency policies. Michigan’s 10 percent renewable electricity standard (RES) ends in 2015, and Governor Snyder recently released a report showing that the state could affordably increase its use of renewable energy to at least 30 percent of the power supply.

In terms of the power providers that own and operate ripe for retirement coal generators, Southern Company holds the top spot with 13,215 MW of coal capacity. That’s more than the next four power providers on the top list (Tennessee Valley Authority, Duke Energy, DTE Energy, and CMS Energy) combined. In January 2013, Southern Company’s subsidiary Georgia Power announced that it would retire 1,976 MW at 10 coal units in the next several years. That’s a good start, but there are many more old, inefficient, and uncompetitive coal units operated by Georgia Power and the rest of Southern Company’s subsidiaries that should also be considered for closure.

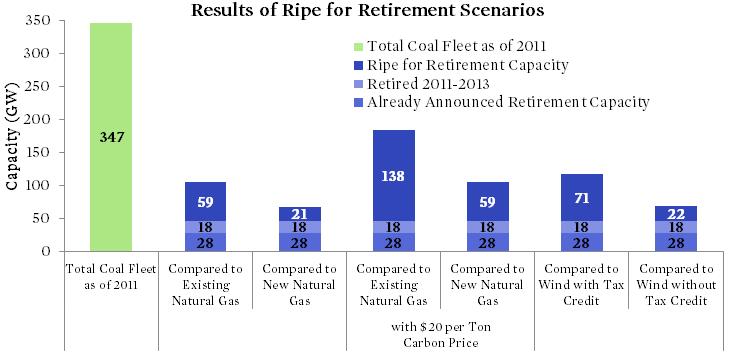

In addition to comparing the coal fleet against natural gas, our analysis examined the competiveness of coal generators with an average new wind power facility, as well as the impact that a $20 per ton price on carbon would have on coal economics. In both cases, we found that a notable increase in the number of ripe for retirement generators (see chart). Stay tuned to the Equation over the next couple of days as two of my UCS colleagues will be discussing more of the findings from both of these comparisons.

The total capacity of ripe for retirement coal generation varies based on the comparison and the presence or absence of a CO2 price and tax credits for wind generation.

Clean and Reliable Replacements for Retiring Coal

The decisions that power providers make today to replace retiring coal plants will determine our electricity sources for decades. Our analysis found that every region of the country has the potential to reliably replace the electricity from ripe-for-retirement coal generators with cleaner alternatives. A combination of projected new renewable energy generation and energy efficiency savings from current state policies, and ramping up underutilized existing natural gas plants can more than replace the combined generation of coal units retired between 2011 and 2013, already slated for retirement, and those identified as ripe for retirement (see chart).

Many utilities are currently replacing much of the generation from retiring coal plants with natural gas. However, if the trend toward natural gas overreliance continues, it will pose serious climate, economic, and public health risks. Instead, a more diversified approach, with dominant roles for renewable energy and energy efficiency, and a more modest role for natural gas, would limit those risks.

Renewable energy and energy efficiency projections are based on projected development through 2020 as a result of existing policy requirements. Potential excess natural gas generation is based on additional generation from ramping up existing NGCC plants to an 85 percent capacity factor.

As utilities, investors, and regulators assess whether cleaner alternatives can more affordably meet customers’ energy needs instead of dumping more ratepayer money into uneconomic coal plants, smart policies are needed to help speed the transition to truly clean energy alternatives. These policies should include a national power plant carbon standard, strong renewable electricity standards and energy efficiency standards, tax credits, investments in research and development, and improved processes for the planning, siting, and financing of needed transmission projects. With thoughtful planning, we can cost-effectively transition to a clean energy economy, while also keeping the lights on.