Allowing renewable energy technologies to be eligible for MLPs would expand the investor base and lower the cost of financing projects by 40 percent or more, according to a new analysis prepared for UCS by Meister Consulting, Inc. (see paper and presentation here).

The analysis also shows that lower financing costs would in turn reduce the all-in cost of generating electricity from wind projects by at least 17 percent (1.2 cents per kilowatt-hour), or about 40 percent of the value of the production tax credit (PTC).

When combined with the PTC and other state and federal renewables policies, MLPs could be an important policy for the U.S. to achieve a clean, low-carbon, energy future.

What are MLPs?

MLPs are a corporate structure that can raise capital by issuing shares of ownership in the stock market, but at the same time enjoy tax benefits not available to typical corporations. While profits from publicly traded corporations are taxed at both the corporate and shareholder levels, income from MLPs is taxed only at the shareholder level because it is treated as a partnership for tax purposes.

Established by Congress in 1980, MLPs have been used extensively by the oil, natural gas, and coal industries. See my blog from April 2013 for more background on MLPs and proposals in Congress that would allow renewables to be eligible, such as the Master Limited Partnerships (MLP) Parity Act.

How big is the MLP market?

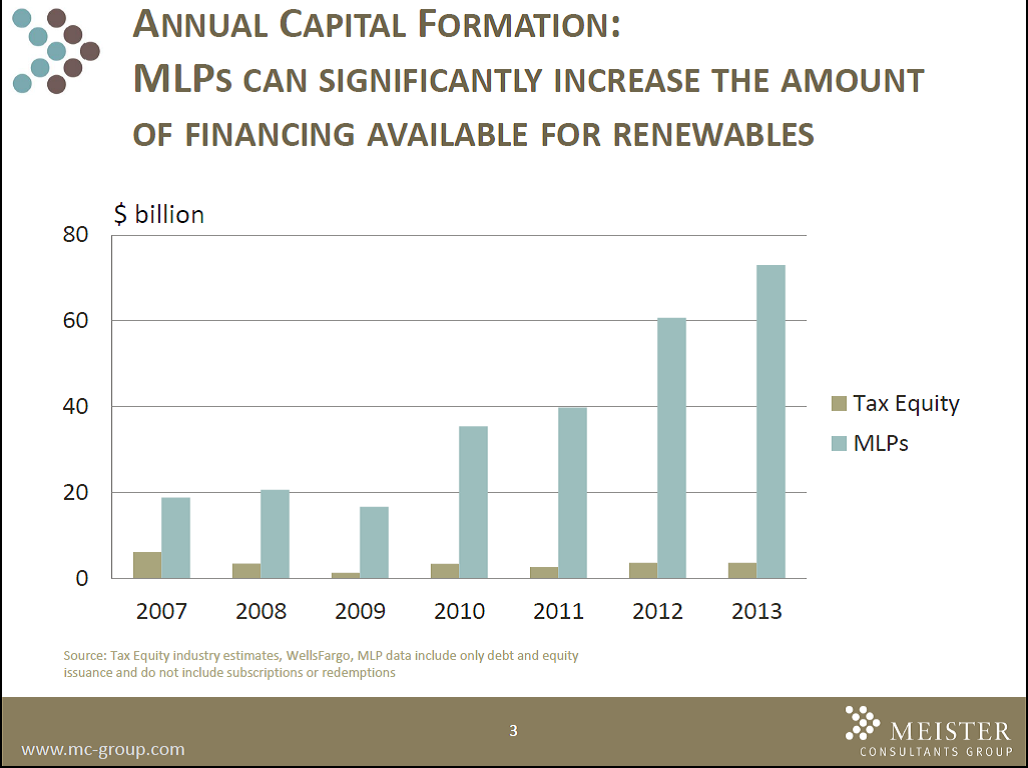

MLPs have grown dramatically over the past six years primarily to fund natural gas and oil pipelines due to the boom in hydraulic fracturing (fracking) of shale deposits in the U.S. The capital flowing into MLPs has exceeded $60 billion per year over the past two years, while the total MLP market capitalization has grown from $96 billion in 2008 to $440 billion in 2013. In stark contrast, tax equity financing for renewable projects has been limited to $3-6 billion per year from a relatively small number of large investment banks and insurance companies.

How much capital is needed to fund renewable energy investments?

In 2012, the renewable energy industry invested more than $40 billion in the U.S. economy, according to Bloomberg New Energy Finance. This included a record-breaking $25 billion to install more than 13,000 MW of wind and $11.5 billion to install more than 3,300 MW of solar (which increased to $13.7 billion and 4,750 MW in 2013).

A 2012 study by the National Renewable Energy Laboratory (NREL) estimates that $50-70 billion per year in capital investment would be required to increase non-hydro renewables to about 30 percent of U.S. electricity generation by 2025, and growing to $85-125 billion per year after 2030 to reach 80 percent renewables (including hydro) by 2050.

While the PTC and other federal climate and energy policies will be needed to achieve this renewable energy future, MLPs could help expand the investor base and unleash a large fraction of low-cost capital required to fund this transition.

Where would the capital come from?

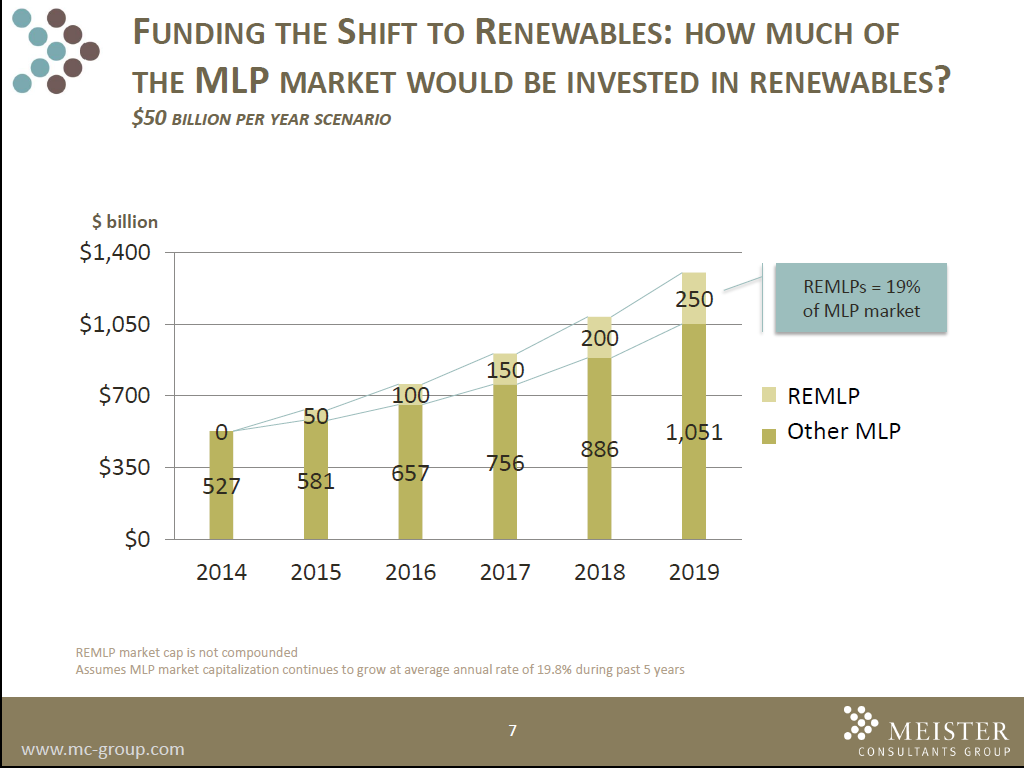

The Meister analysis identified two segments of potential investors in renewable energy MLPs (RE-MLPs) – the $15 trillion U.S. mutual fund market and the $11 trillion U.S. defined-benefit pension market. They found that these investors are drawn to MLPs by the prospects of high income generation compared to very low rates in bonds and disappointing returns in alternative asset classes.

The analysis found that using MLPs to finance renewables at $50-70 billion per year over the next five years would only require a shift of 0.7 to 1 percent of the total portfolio of these asset classes. Under this scenario, RE-MLPs would represent less than 20 percent of the total MLP market. While other sources of financing would also be available, it clearly demonstrates that the MLP market could provide a significant share and the pool of potential investors is enormous.

How does this affect the cost of capital?

Tax equity investors currently target an average return of about 11 percent for renewable energy projects. For MLP pricing, the Meister analysis identified three asset types with similar characteristics and varying credit quality, and found that the best proxy for RE-MLPs would be lower quality investment grade (BBB-) natural gas pipeline deals, which currently trade at about 4.9 percent.

Based on this, they found that RE-MLPs may reasonably be expected to converge from the current level of 11 percent equity, or an 8 percent weighted average cost of capital based on a mix of equity and debt financing, to something approaching 4.9 percent over five years.

Using NREL’s Cost of Renewable Energy Spreadsheet (CREST) Tool, UCS analysis found that by lowering the cost of capital by just 3 percent, MLPs could lower the 20-year levelized cost of electricity for a typical wind project by 17 percent (1.2 cents/kWh) compared to traditional financing without the PTC. This finding is consistent with a recent NREL analysis. At this level, MLPs would be worth 41 percent of the value of the PTC, as shown in the chart.

MLPs are an important complement to other renewable energy policies

By giving renewable energy projects access to a much larger pool of investors and lower cost financing, MLPs help address a specific market barrier that’s currently inhibiting development. In this way, they provide an important complement to other policies such as federal tax credits and state renewable electricity standards, which have been the primary drivers of renewable energy development in the U.S.

MLPs have played a similar role in the oil, gas, and coal industries over the past 30 years by supplementing dozens of other federal and state tax incentives available to those industries. For example, shale gas developers have received approximately $10 billion in tax credits, and millions in research and development funding, that have helped fuel the shale gas revolution.

In early April, I had the chance to hear Senator Wyden (D-OR) — Chair of the Senate Finance Committee — speak at the Bloomberg New Energy Finance summit in New York City about the need to revise the U.S. tax code to provide “parity and predictability” for energy investments. He highlighted extending the PTC and allowing renewables to be eligible for MLPs as two important policies that meet these goals.